Secure Your Home with Top-Rated Home Insurance

Secure Your Home with Top-Rated Home Insurance

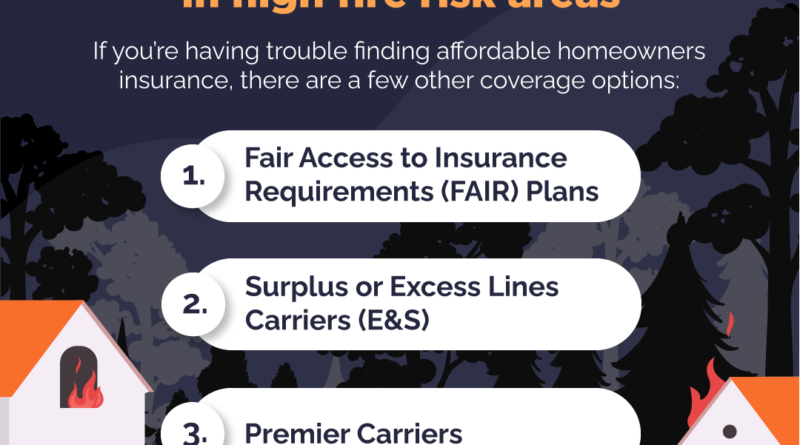

In the contemporary landscape of homeownership, securing adequate home insurance is paramount for safeguarding personal investments against an array of risks. As natural disasters become increasingly prevalent, the necessity of comprehensive insurance coverage is underlined by research that reveals homeowners often face significant barriers to effective risk mitigation, including perceptions of necessity and inconvenience ((Lee et al.)). Furthermore, these challenges are compounded by the financial implications of extreme weather, prompting homeowners to seek alternative insurance options tailored to their specific circumstances ((Webb P et al.)). Visual aids, such as , highlight the evolving options available for homeowners in disaster-prone areas, illustrating how insurance solutions can be strategically aligned to address the unique vulnerabilities each household faces. Thus, understanding the importance of top-rated home insurance is crucial, not only for financial security but also for fostering a proactive approach to home safety and risk management.

A. Importance of Home Insurance in Protecting Assets

Home insurance serves as a critical safeguard for individuals looking to protect their most significant asset: their home. This type of insurance not only provides financial support in the event of damages from natural disasters, theft, or accidents, but it also fosters a sense of security and stability in uncertain times. Given the increasing risks associated with climate change and evolving regulatory environments, such as those identified in recent studies regarding food security and risk management in Australia (Michael D et al.), homeowners must be proactive in securing their properties. Furthermore, the evolving landscape necessitates an understanding of available resources that might assist policyholders, particularly those in high-risk areas, as illustrated by . Home insurance thus emerges as an essential mechanism, integrating both financial protection and peace of mind in a world marked by unpredictability, akin to observations made in the financial industry throughout various economic downturns (Devine et al.).

| Coverage Type | Description | Typical Coverage Amount | Examples of Coverage |

| Dwelling Coverage | Protects the structure of your home | 100% of home’s rebuilding cost | Damage from fire, wind, hail |

| Personal Property | Covers your belongings inside the home | 50-70% of dwelling coverage | Furniture, clothing, electronics |

| Liability Protection | Covers legal expenses if someone is injured on your property | $100,000 to $500,000 | Guest slips and falls, dog bites |

| Additional Living Expenses | Covers costs if you can’t live in your home due to covered damage | 20-30% of dwelling coverage | Hotel stays, restaurant meals |

| Other Structures | Covers structures not attached to your home | 10% of dwelling coverage | Detached garage, fence, shed |

II. Understanding Home Insurance Policies

Navigating the complexities of home insurance policies is crucial for homeowners seeking adequate protection against potential financial losses. Policies are typically categorized into various types, each with distinct coverage levels, including dwelling, personal property, liability, and additional living expenses. Understanding these categories is essential for identifying the right policy that fits individual needs, particularly in high-risk areas prone to natural disasters. For instance, homeowners in regions vulnerable to wildfires might consider alternatives like FAIR Plans or Surplus Lines Carriers that address their unique coverage challenges, as depicted in . Furthermore, as demonstrated in studies of labor markets, professionals, including insurance agents, face pressures to standardize offerings which may limit available options for clients, indicating a need for informed consumer advocacy in assessing policies effectively (Webb P et al.), (Hyman et al.). Ultimately, comprehending these components allows for informed decision-making, ensuring secure and efficient home insurance investments.

A. Types of Coverage Offered by Home Insurance

Understanding the types of coverage offered by home insurance is paramount for homeowners seeking effective protection. Home insurance typically encompasses several key areas of coverage, including dwelling coverage, which protects the physical structure of the home, and personal property coverage, which insures the contents against risks such as theft or damage. Liability coverage is another critical component, safeguarding homeowners against legal claims related to injuries or damages incurred on their property. In regions prone to natural disasters, additional endorsements like flood or earthquake coverage may be necessary for comprehensive protection. The significance of such specialized coverage is illustrated in , which highlights the options available for those in areas vulnerable to fire hazards. By understanding these diverse coverage types, homeowners can select insurance that aligns with their specific needs, ultimately enhancing their peace of mind and financial security in an unpredictable world (N/A), (N/A).

III. Choosing the Right Home Insurance

When navigating the complex landscape of home insurance, distinguishing between various policy types is essential for securing adequate coverage. It is vital to consider factors such as the likelihood of natural disasters in your area, the value of your possessions, and the specific risks that may apply to your home. The evolving dynamics of climate change have necessitated innovative insurance solutions, particularly in regions susceptible to wildfires. For instance, the guidance presented in offers alternatives for those struggling to find affordable homeowners insurance, showcasing options like FAIR Plans and Premier Carriers. Understanding these choices can help homeowners avoid gaps in coverage, which could lead to significant financial strain during unforeseen events. Moreover, seeking expert advice on finance and debt management can further mitigate risk while enhancing one’s ability to make informed decisions about insurance, as noted in (Davis K et al.) and (Department CA).

A. Factors to Consider When Selecting a Policy

When selecting a home insurance policy, various factors warrant careful consideration to ensure comprehensive coverage and financial security. One critical aspect is the regional risk associated with natural disasters, such as hurricanes and floods, which can significantly influence insurance premiums and availability. Research indicates that consumers are responsive to the availability of coverage options, particularly in disaster-prone areas (Martin F Grace et al.). Furthermore, the role of state regulations and guaranty funds can affect policy choice, providing reassurance to homeowners against insurer insolvency (Martin F Grace et al.). Understanding the nuances of policy terms, such as deductibles and limits of liability, is essential, as these elements directly impact the out-of-pocket costs during claims. As homeowners increasingly seek automated resources for assistance, studies find consistency in the accuracy of AI-generated information regarding insurance, particularly highlighting its relevance for climate-related hazards . Thus, these elements collectively inform wiser policy selection, enhancing protection against potential risks. Incorporating tools like can visually aid homeowners in navigating these complex decisions.

Securing your home with top-rated home insurance is not merely a financial decision; it embodies a proactive stance towards safeguarding ones assets and peace of mind. The unpredictability of natural disasters and unforeseen events underscores the necessity for robust insurance coverage that adapts to evolving risks, as demonstrated through insights gathered from various studies (Davis K) and (Takach M et al.). The visual representation in effectively highlights the challenges homeowners face in high-risk areas, offering valuable alternatives for securing coverage. As homeowners increasingly recognize the critical benefits of comprehensive insurance policies, it becomes paramount to engage with trusted providers and tailor insurance options to fit individual circumstances. Ultimately, a well-structured home insurance policy provides both financial security and emotional reassurance, ensuring that homeowners are equipped to navigate lifes uncertainties.

A. The Long-Term Benefits of Investing in Quality Home Insurance

Investing in quality home insurance is not merely a precaution; it is a strategic decision with long-lasting benefits for homeowners. Quality coverage protects against unforeseen disasters, preserving not only the physical structure of the home but also the emotional and financial stability of families. Over time, the peace of mind that accompanies comprehensive coverage allows homeowners to focus on other aspects of life without the constant worry of potential losses. Moreover, a robust insurance policy can facilitate faster recovery after an incident, minimizing downtime and financial strain. The long-term savings associated with well-designed insurance plans often outweigh initial costs, providing families with reliable support through challenging times. As noted by experts at the Financial Innovations Roundtable, understanding the nuances of home insurance can significantly influence decision-making towards securing a safe and stable living environment (Giszpenc et al.). In this way, quality home insurance stands as a crucial investment in personal and financial security (N/A).