How Do Life Insurance Companies Make Money? The Morbid Math Behind the Business – SSunnel

Life insurance is one of those things that most people know they should have but don’t fully understand. It’s a safety net, a way to ensure that your loved ones are financially protected if something happens to you. After all, everyone dies eventually, so how do these companies stay profitable? The answer lies in a mix of statistics, investments, and carefully crafted contracts. Let’s break it down.

What Is Life Insurance?

You pay regular premiums, and in return, the company promises to pay out a death benefit to your chosen beneficiaries when you pass away. This payout can help cover funeral costs, replace lost income, pay off debts, or provide financial stability for your family.

But here’s the question: if everyone dies eventually, how do life insurance companies avoid going bankrupt? The answer lies in the types of policies they offer and how they manage risk.

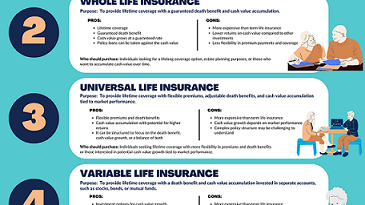

The Two Main Types of Life Insurance

Each works differently, and understanding these differences is key to seeing how insurance companies turn a profit.

1.Term Life Insurance

If you die during that term, the insurance company pays out the death benefit to your beneficiaries.

For example, let’s say you buy a 20-year term life policy with a

500,000 death benefit.If Passaway within those 20 years,your family receives 500,000. If you’re still alive at the end of the term, the policy ends, and the insurance company keeps all the premiums you paid.

This is where the insurance company starts to make money. They use actuarial science—basically, a mix of math and statistics—to predict how many people in a group will die during the term. By setting premiums based on these predictions, they ensure that the total payouts are less than the total premiums collected.

Here’s a simplified example:

100 people each pay $50 per month for a 10-year term life policy.

Over 10 years, the insurance company collects $600,000 in premiums.

If only 25 of those people die during the term, the company pays out

500,000(assuming each policy has a 20,000 death benefit).

That leaves the company with a $100,000 profit, not including any money they made by investing the premiums in the meantime.

2.Permanent Life Insurance

As long as you keep paying your premiums, the policy will pay out whenever you die. This type of insurance is more expensive than term life, but it also includes a savings or investment component, known as cash value.

So how do insurance companies make money on permanent policies?

Lapsed Policies: Many people stop paying their premiums at some point, especially if they can no longer afford them. When this happens, the insurance company keeps all the premiums paid up to that point and doesn’t have to pay out a death benefit.

Investments: Insurance companies invest the premiums they collect. Over time, these investments can grow significantly, thanks to compound interest. For example, if a 20-year-old pays 70 per month for a 100,000 policy and lives to be 80, they’ll have paid $50,000 in premiums. If the insurance company invested that money at a modest interest rate, it could grow to several hundred thousand dollars by the time the policy pays out.

Higher Premiums: Permanent life insurance policies are more expensive than term life policies, which means the company collects more money upfront.

The Role of Actuarial Science

At the heart of the life insurance business is actuarial science. Actuaries are professionals who use math, statistics, and financial theory to assess risk. They analyze data to predict how many people in a given group will die within a certain time frame and set premiums accordingly.

For example, a healthy 30-year-old is less likely to die in the next 20 years than a 60-year-old with health issues. As a result, the 30-year-old will pay lower premiums for the same coverage. By carefully assessing risk, insurance companies can ensure that they collect enough premiums to cover payouts while still making a profit.

Investing Your Premiums

One of the biggest ways life insurance companies make money is by investing the premiums they collect. While they hold onto your money, they invest it in stocks, bonds, real estate, and other assets. Over time, these investments can generate significant returns.

Fine Print and Loopholes

Another way life insurance companies protect their profits is by including specific terms and conditions in their policies. For example:

Suicide Clauses: Many policies won’t pay out if the policyholder dies by suicide within the first two years of the policy.

Exclusions: Some policies exclude deaths caused by risky activities, like skydiving or drug use.

Lapse Policies: If you stop paying your premiums, the company can cancel your policy and keep all the money you’ve paid.

These clauses help insurance companies avoid paying out in certain situations, further protecting their bottom line.

Why Buy Life Insurance?

With all this talk of profits and payouts, you might be wondering: why even buy life insurance? The answer is simple: peace of mind. Life insurance ensures that your loved ones are financially protected if something happens to you.

For example, if you’re the primary breadwinner in your family, your death could leave your spouse and children struggling to pay the mortgage, cover living expenses, or fund education. A life insurance payout can help bridge that gap and provide stability during a difficult time.

Even if you don’t have dependents, life insurance can cover funeral costs, pay off debts, or leave a legacy for a cause you care about.

The Bottom Line

Life insurance companies make money by carefully managing risk, investing premiums, and setting terms that protect their profits. While it might seem like a morbid business, it’s also a necessary one. Life insurance provides financial security for millions of families, ensuring that they’re taken care of even after a loved one is gone.

So, the next time you pay your life insurance premium, remember: you’re not just buying a policy—you’re investing in peace of mind for yourself and your loved ones. And while the insurance company might be making a profit, the real value lies in the protection and security it provides.

After all, life is unpredictable, but with the right insurance, you can face the future with confidence.